Page 10 - Mines and Minerals Reporter eMagazine - Volume October 2021

P. 10

INDUSTRY ANALYSIS

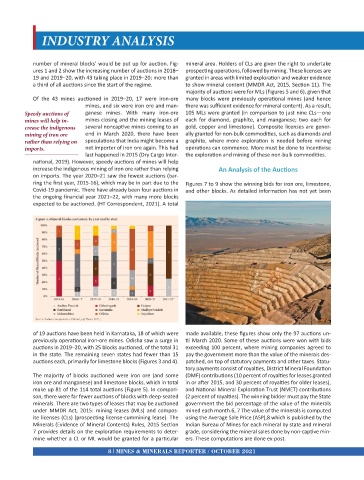

number of mineral blocks’ would be put up for auction. Fig- mineral area. Holders of CLs are given the right to undertake

ures 1 and 2 show the increasing number of auctions in 2018– prospecting operations, followed by mining. These licenses are

19 and 2019–20, with 43 taking place in 2019–20; more than granted in areas with limited exploration and weaker evidence

a third of all auctions since the start of the regime. to show mineral content (MMDR Act, 2015, Section 11). The

majority of auctions were for MLs (Figures 5 and 6), given that

Of the 43 mines auctioned in 2019–20, 17 were iron-ore many blocks were previously operational mines (and hence

mines, and six were iron ore and man- there was sufficient evidence for mineral content). As a result,

Speedy auctions of ganese mines. With many iron-ore 105 MLs were granted (in comparison to just nine CLs—one

mines will help in- mines closing and the mining leases of each for diamond, graphite, and manganese; two each for

crease the indigenous several noncaptive mines coming to an gold, copper and limestone). Composite licenses are gener-

mining of iron ore end in March 2020, there have been ally granted for non-bulk commodities, such as diamonds and

rather than relying on speculations that India might become a graphite, where more exploration is needed before mining

imports. net importer of iron ore again. This had operations can commence. More must be done to incentivise

last happened in 2015 (Dry Cargo Inter- the exploration and mining of these non-bulk commodities.

national, 2019). However, speedy auctions of mines will help

increase the indigenous mining of iron ore rather than relying An Analysis of the Auctions

on imports. The year 2020–21 saw the fewest auctions (bar-

ring the first year, 2015-16), which may be in part due to the Figures 7 to 9 show the winning bids for iron ore, limestone,

Covid-19 pandemic. There have already been four auctions in and other blocks. As detailed information has not yet been

the ongoing financial year 2021–22, with many more blocks

expected to be auctioned. (HT Correspondent, 2021). A total

of 19 auctions have been held in Karnataka, 18 of which were made available, these figures show only the 97 auctions un-

previously operational iron-ore mines. Odisha saw a surge in til March 2020. Some of these auctions were won with bids

auctions in 2019–20, with 25 blocks auctioned, of the total 31 exceeding 100 percent, where mining companies agreed to

in the state. The remaining seven states had fewer than 15 pay the government more than the value of the minerals des-

auctions each, primarily for limestone blocks (Figures 3 and 4). patched, on top of statutory payments and other taxes. Statu-

tory payments consist of royalties, District Mineral Foundation

The majority of blocks auctioned were iron ore (and some (DMF) contributions (10 percent of royalties for leases granted

iron ore and manganese) and limestone blocks, which in total in or after 2015, and 30 percent of royalties for older leases),

make up 81 of the 114 total auctions (Figure 5). In compari- and National Mineral Exploration Trust (NMET) contributions

son, there were far fewer auctions of blocks with deep-seated (2 percent of royalties). The winning bidder must pay the State

minerals. There are two types of leases that may be auctioned government the bid percentage of the value of the minerals

under MMDR Act, 2015: mining leases (MLs) and compos- mined each month.6, 7 The value of the minerals is computed

ite licenses (CLs) (prospecting license-cummining lease). The using the Average Sale Price (ASP),8 which is published by the

Minerals (Evidence of Mineral Contents) Rules, 2015 Section Indian Bureau of Mines for each mineral by state and mineral

7 provides details on the exploration requirements to deter- grade, considering the mineral sales done by non-captive min-

mine whether a CL or ML would be granted for a particular ers. These computations are done ex-post.

8 MINES & MINERALS REPORTER / OCTOBER 2021